Reversion Signals Light Up, While Risk On Remains Intact: Caltropia Signals Report May 8th

Reversion Signals have been lighting up, risk on remains intact, and more. Check out our weekly update for the upcoming week

Caltropia Market Terminal Article

Free Caltropia Research Market Terminal Dashboard

View all the signals and regimes at the Terminal Dashboard Link above for free, in a more intuitive and actionable format. Some below Dash’s are still in dev, and will be released shortly. I tried to get this out earlier today, but had difficulty with internet and backend data populating.

Intro Summary

Quick update, we are going to add many more equity signals shortly, however, there are many potential issues with this and how we do so. The data for these equity signals is doable in terms of cost. However, the other data we need for other equity signals we have is quite expensive. Therefore, the best way to do this is to first get the signals we can. However, to keep them separate from all other databases and signals etc. Therefore, it’s possible that next week you will see more equity signals, however, until we get the data for other equity signals these will be reported separately and not included in the models as we don’t want to contaminate them.

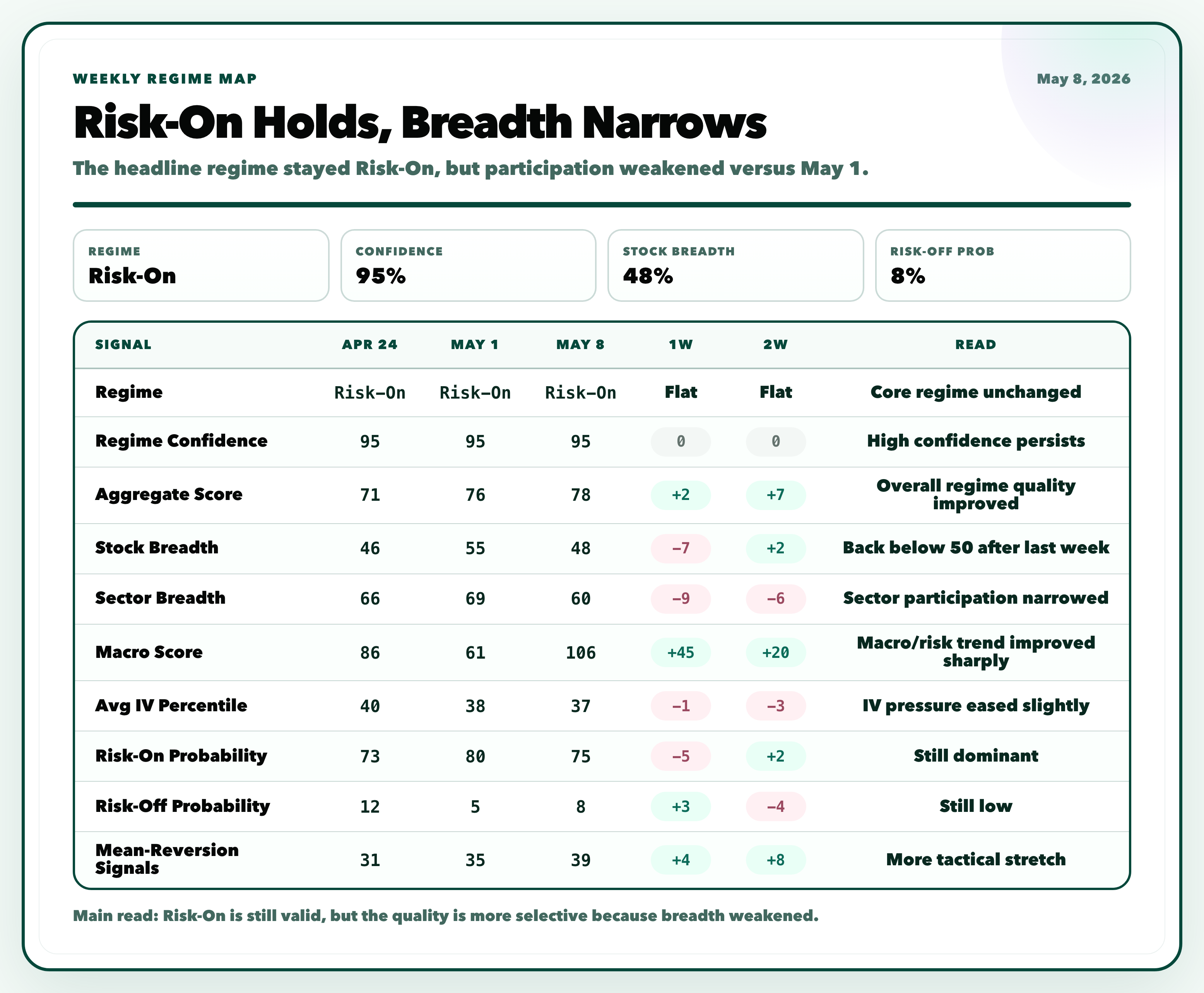

Our full signal stack remains Risk On, but the underlying character of the signal changed this week.

The main regime model is still in Risk On with 95 confidence. The aggregate score improved again, moving from 71 on April 24, to 76 on May 1, to 78 on May 8. The macro score also improved sharply this week, moving from 61 last Friday to 106 now. So the headline regime is still looking good.

The important thing though is breadth. Stock breadth fell from 55 last Friday to 48 now, and sector breadth fell from 69 to 60. That means this week was not a clean broadening week as we would like to see. We would like to see the broadening continue after last week’s increase.

The model still says Risk On, but participation narrowed after last week’s improvement. The regime is still supportive, but the tape is not as broadly healthy as it was last Friday and actually weakened.

The historical regime proxy is also still Risk On. It has improved from the borderline Risk On reading on April 24 to a much cleaner Risk On snapshot now. The SPY realized vol percentile has also fallen meaningfully, from 84.1 on April 24, to 45.2 on May 1, to 37 now. That is important because it’s saying the historical analog layer is no longer being dragged down by the high vol backdrop we had in the data two weeks ago.

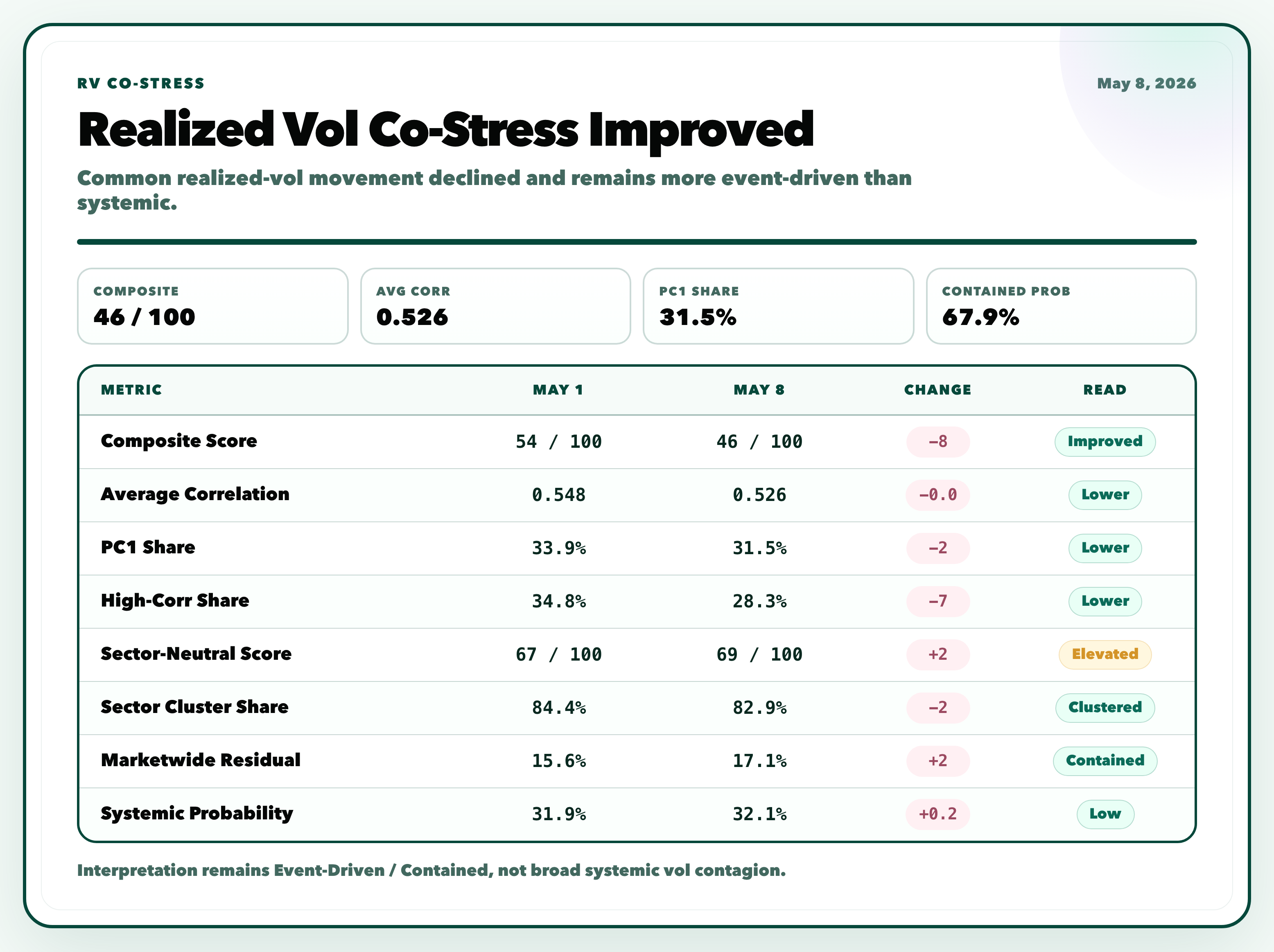

The volatility signal stack is mostly supportive as well. Systemic Vol Contagion is still contained at 39, Forward Risk State Composite is contained at 44, and Compression to Expansion fell from 35 last Friday to only 12 now, however, is still not 0. Regardless, that is an improvement versus last week’s main yellow flag. Realized vol co stress also improved, with the composite falling from 54 to 46.

One caveat is that the market is still not completely clean. Calm at Risk is at 47, which is lower than last Friday but still elevated in percentile terms. Mean reversion signals increased even further from 35 to 39, and stock breadth is back below 50. So this is still Risk On, but it is even more selective than last week.

Summary

The market remains Risk On, volatility risk is still contained, and the most important systemic vol signals are not flashing panic, but flashing tiny signs, but nothing statistically significant. Breadth narrowed, mean reversion stretch increased, and the market is more dependent on selective leadership than it was last Friday which is worrying.

What Changed Since The Last Two Fridays

Overall regime quality improved, Stock Breadth, is back below 50 after last week’s improvement. Sector Breadth and Sector participation narrowed with the Macro Score improving sharply. Mean Reversion is showing more tactical stretch under the surface, with Stock Dispersion slightly more uneven and Sector Dispersion still dispersed, but less than last week.

The most important change is the split between regime and breadth. The regime model improved slightly, but breadth did not which we would have liked to see. This matters because a Risk On regime with rising breadth is cleaner than a Risk On regime with narrowing participation. This week’s read is therefore again selective and the model is still constructive, but the market is not giving us the same breadth confirmation that it gave last Friday and I would have loved to see this week.

Market Regime

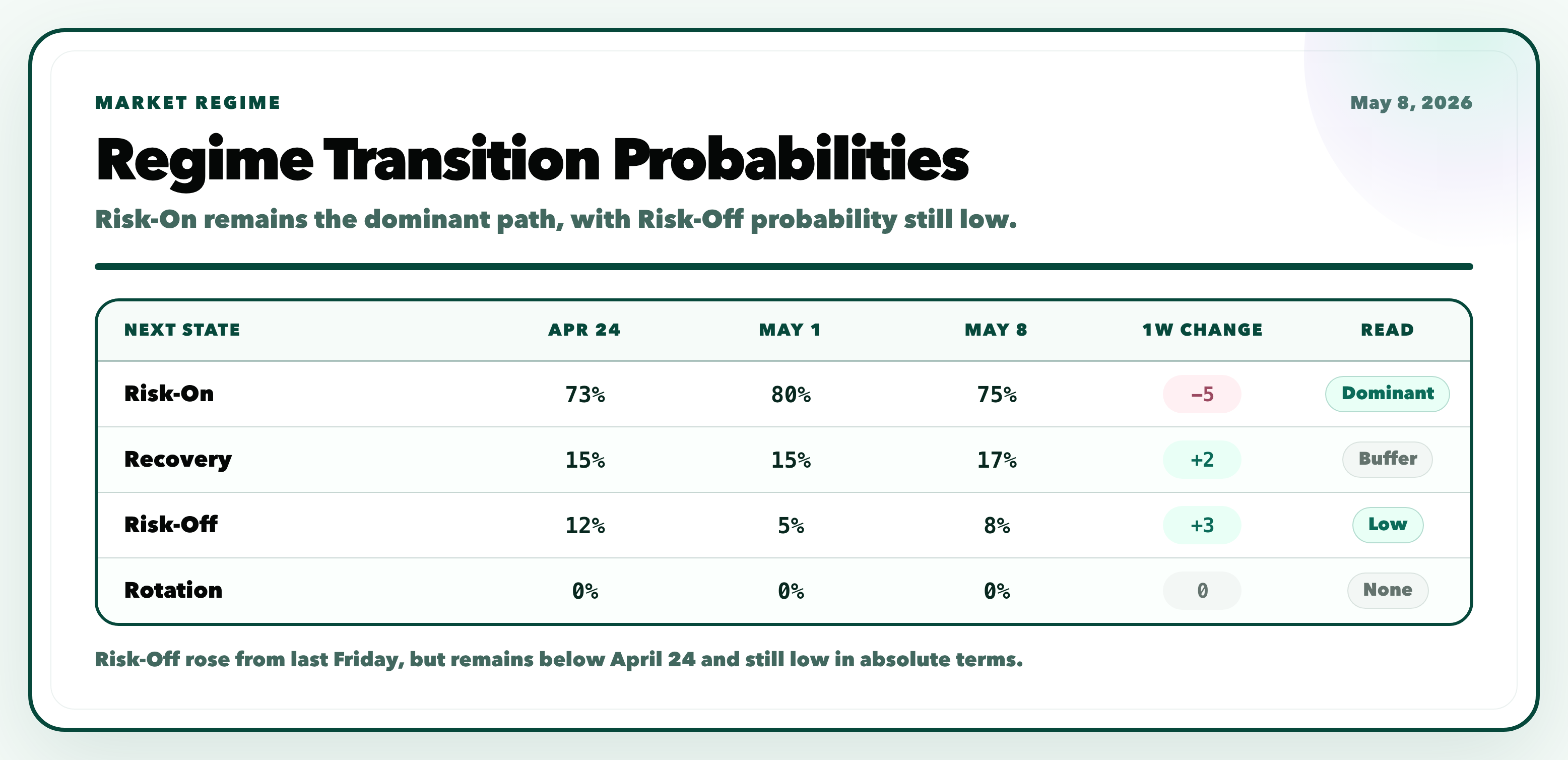

The market remains in Risk On Regime.

Current regime transition probabilities are as follows in the above table: This is still a nice transition profile. Risk On remains the dominant state, Risk Off probability is still low, and there is no rotation signal.

The useful internal details are:

Aggregate score improved from 76 to 78.

Macro score improved from 61 to 106.

Average IV percentile eased from 38 to 37.

Stock breadth fell from 55 to 48.

Sector breadth fell from 69 to 60.

Mean-reversion signals rose from 35 to 39.

Risk On remains the base case, but the quality of the move narrowed which is not a positive development. The model is not showing a broad Risk Off transition, but breadth is weaker than it was last Friday.

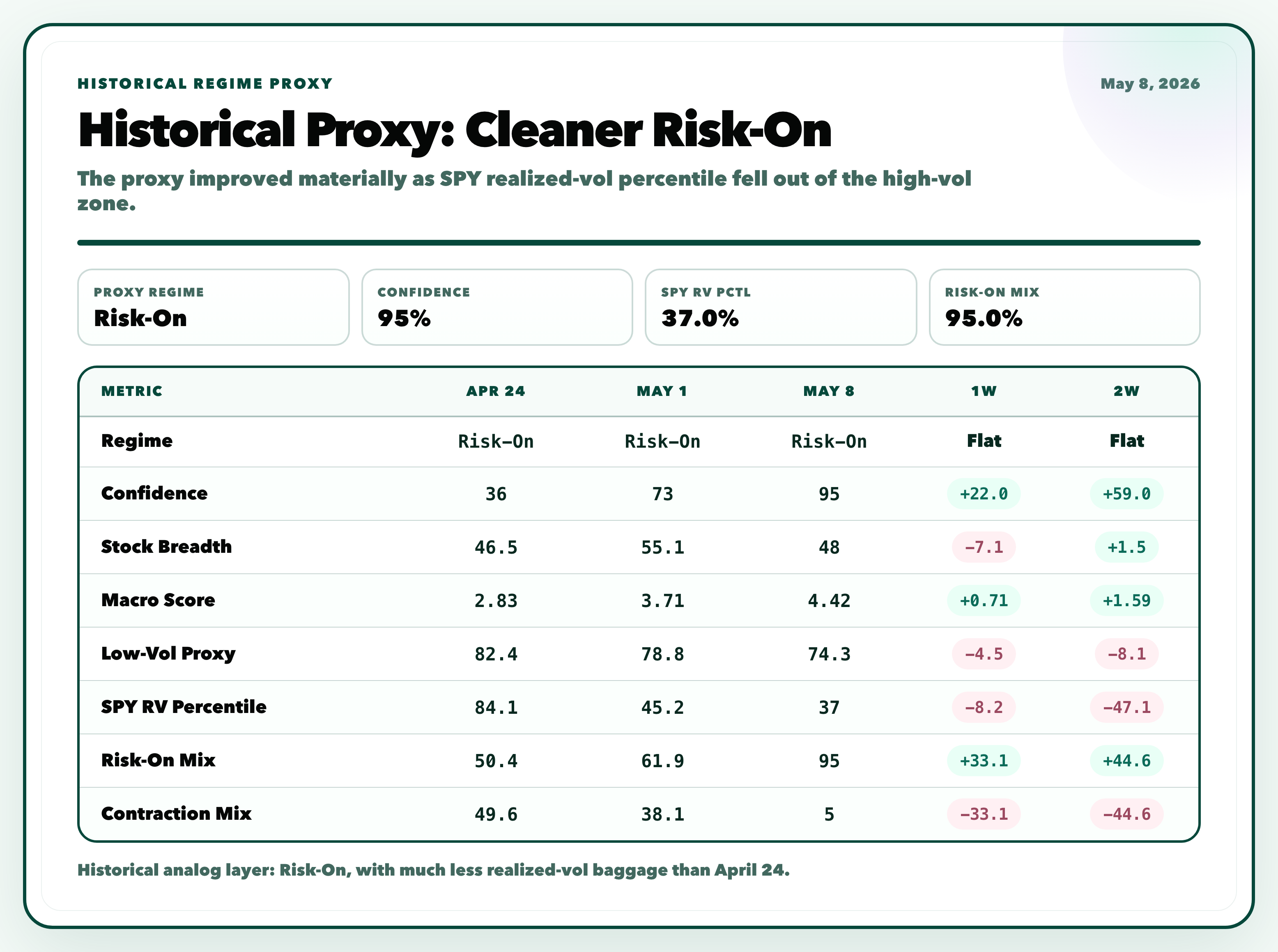

Historical Regime Proxy

The historical analog layer is also Risk On. This layer has improved a lot over the last two weeks. On April 24, the historical proxy was technically Risk On, but only barely. Confidence was 36, and SPY realized vol percentile was still very high at 84.1.

Now the proxy is much cleaner. Confidence is 95, macro score improved, and SPY realized vol percentile has fallen to 37. That means the analog layer is no longer saying “Risk On, but with very high realized vol baggage.” It is saying “Risk-On with a calmer vol backdrop.” The caveat is the same as the main model, however, stock breadth slipped back below 50. So the historical analog is cleaner on volatility, but less clean on participation. Remember this is a slower moving Model than the Main one above.

Trend States

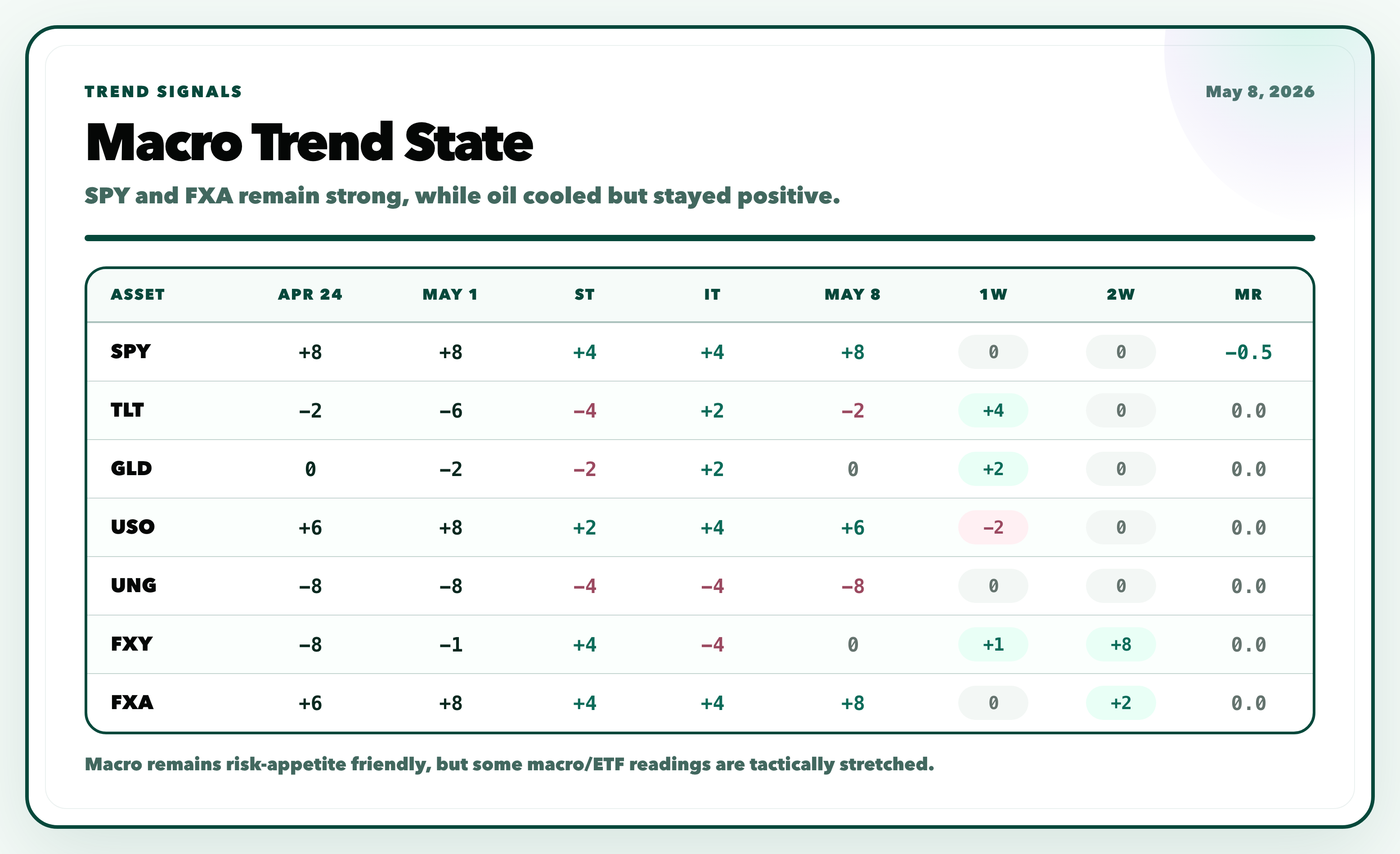

The main macro trend signals remain, but the leadership mix changed.

SPY remains strongly positive at +8. Which is important because the headline equity trend is still intact. The Australian dollar is also strong at +8, which supports the risk appetite read.

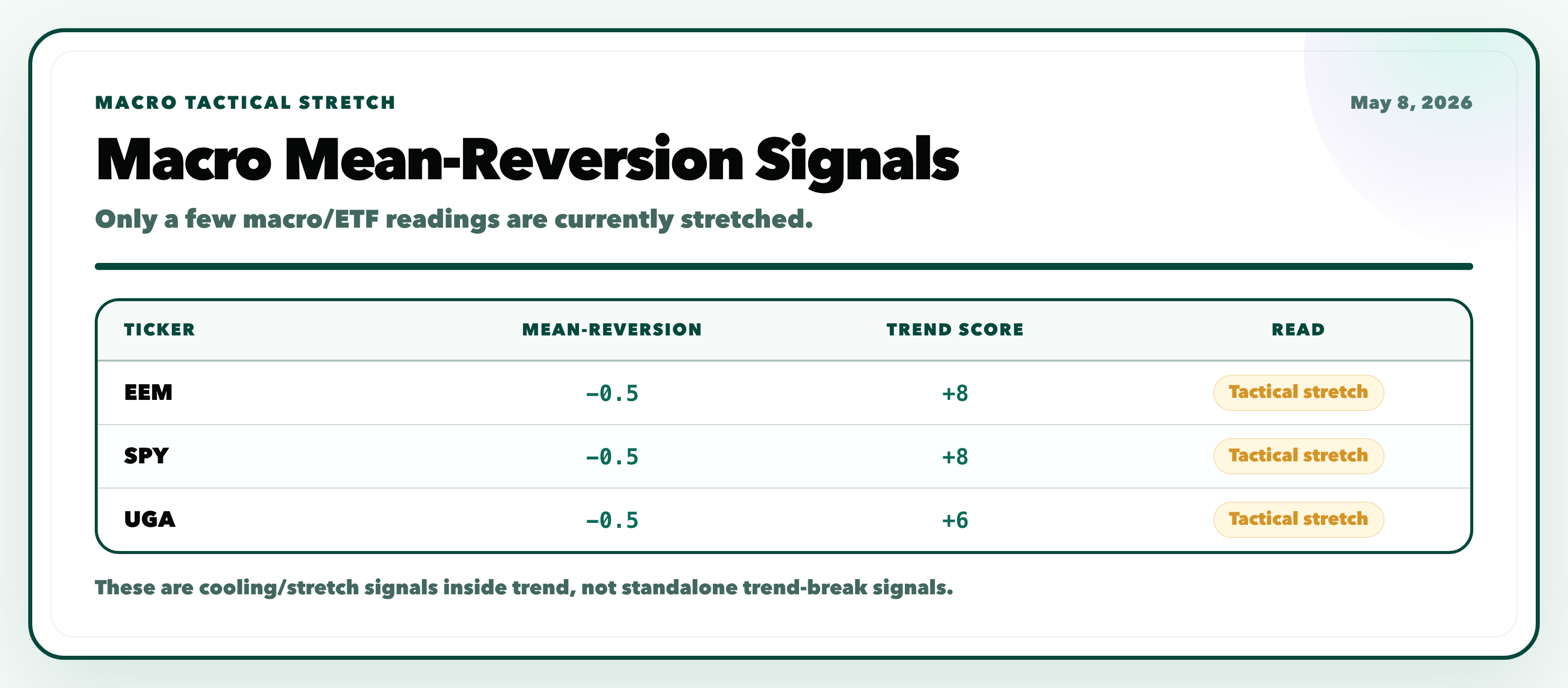

Oil cooled from +8 to +6, but remains positive. Bonds improved from last week but are still slightly negative on the combined trend score. Gold moved back to neutral. Yen improved materially from two weeks ago with the CB intervening in the Yen, with short term strength now positive, but the intermediate trend is still weak.

Macro mean reversion is mild and mostly concentrated in risk assets/commodities. Remember these are not saying the trend is broken. It says the market is still trending, but parts of the macro tape are tactically stretched and need to revert.

Volatility Regime

The volatility dashboard currently has 140 names in the universe. The broad volatility picture is still contained. | Vol Metric | May 8 | Total tickers | 140 | | Names with VRP | 138 | | Median RV | 22.63% | | Median IV | 33.50% | | Median VRP | 0.53 | | Mean VRP | 0.54 | | Buy-vol candidates | 20 | | Sell-vol candidates | 22 | | Negative VRP share | 0.0% | | VRP compression score | 68 | | Vol breadth stress score | 22 | This is not a stressed volatility cross section. Median VRP remains positive, negative VRP share is still 0.0%, and implied vol is not showing broad panic.

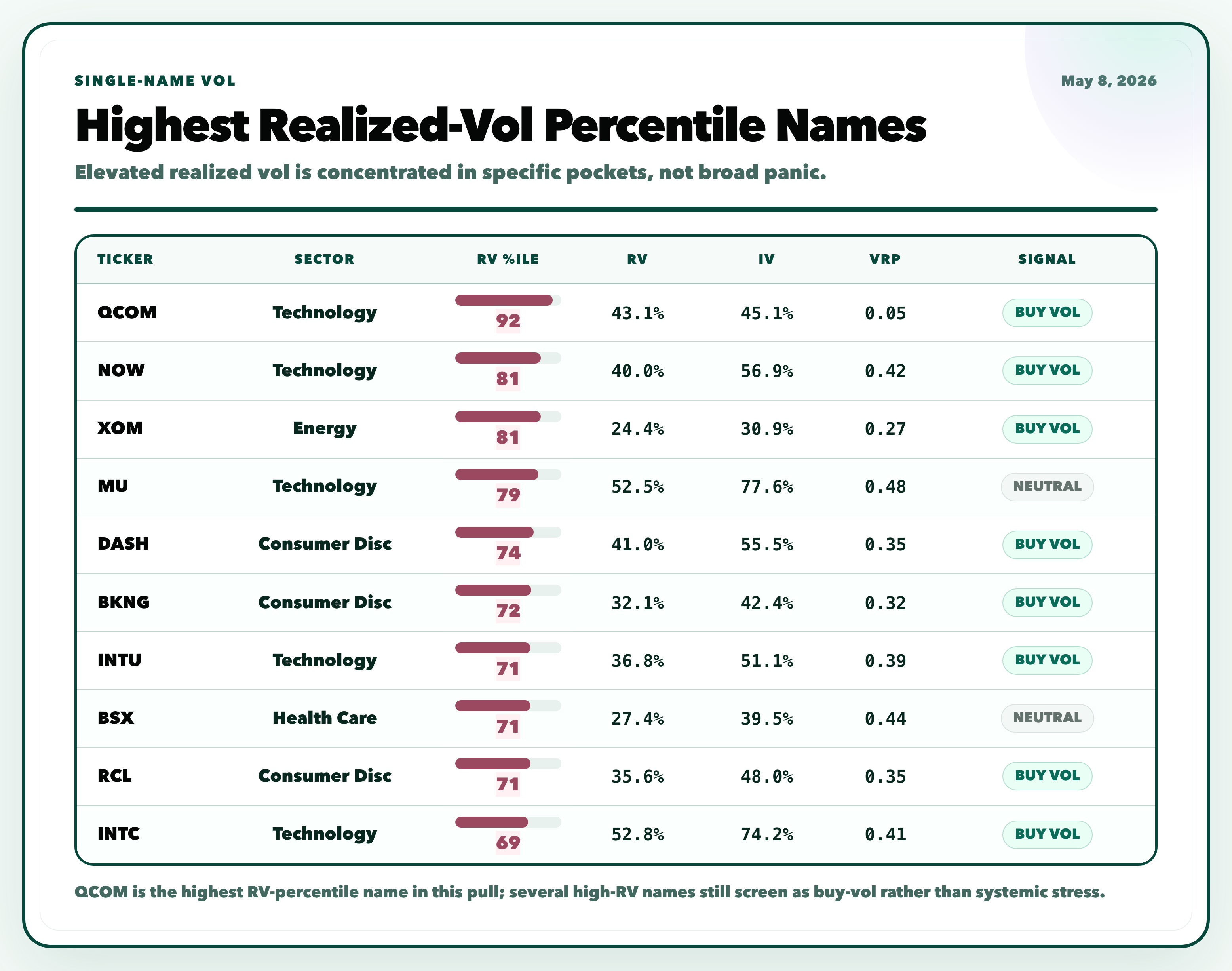

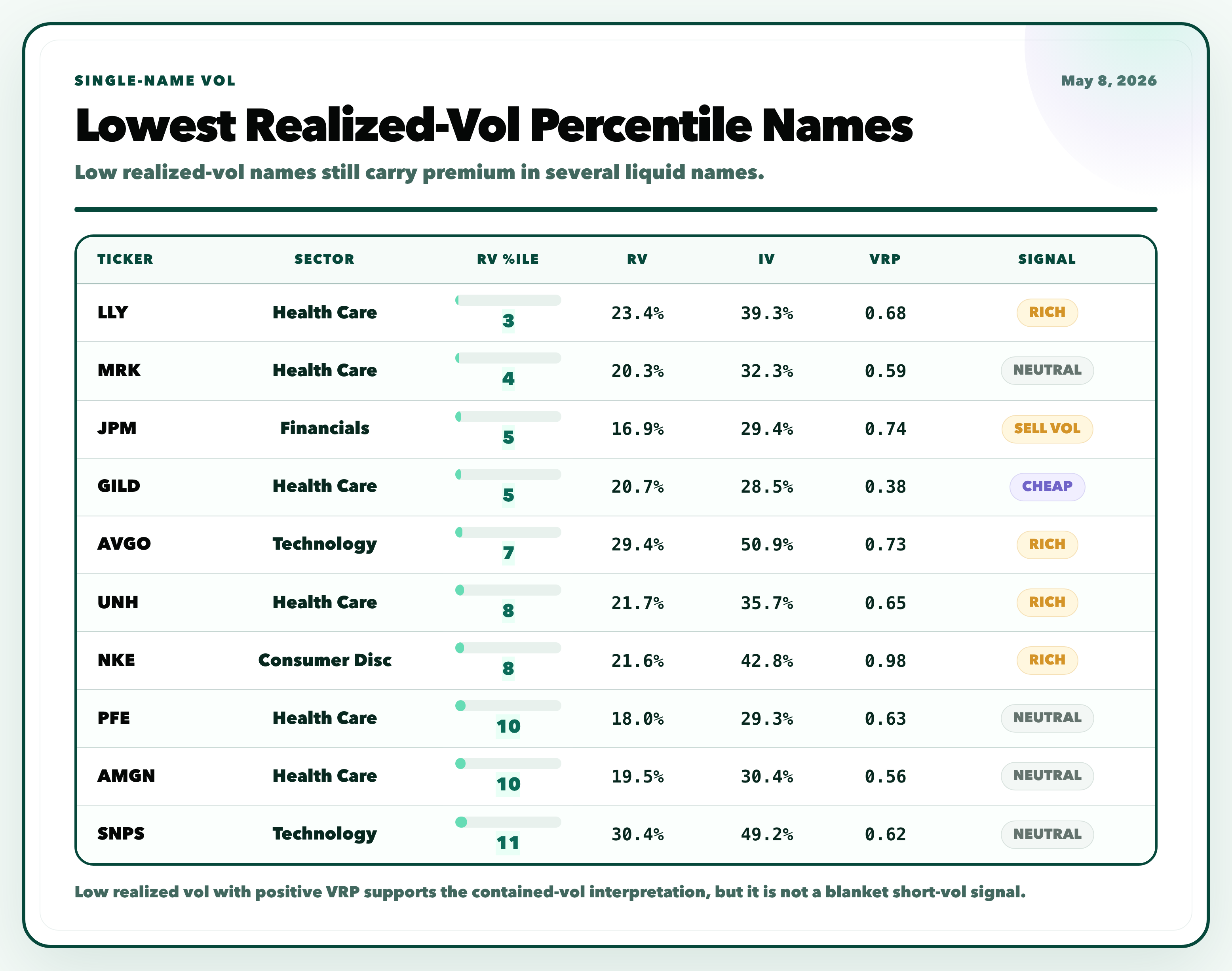

The highest realized vol percentile names above: The interesting part is that realized volatility remains low in several large liquid names while implied vol still carries a premium. That is consistent with a market where realized stress is contained, but options are not completely complacent.

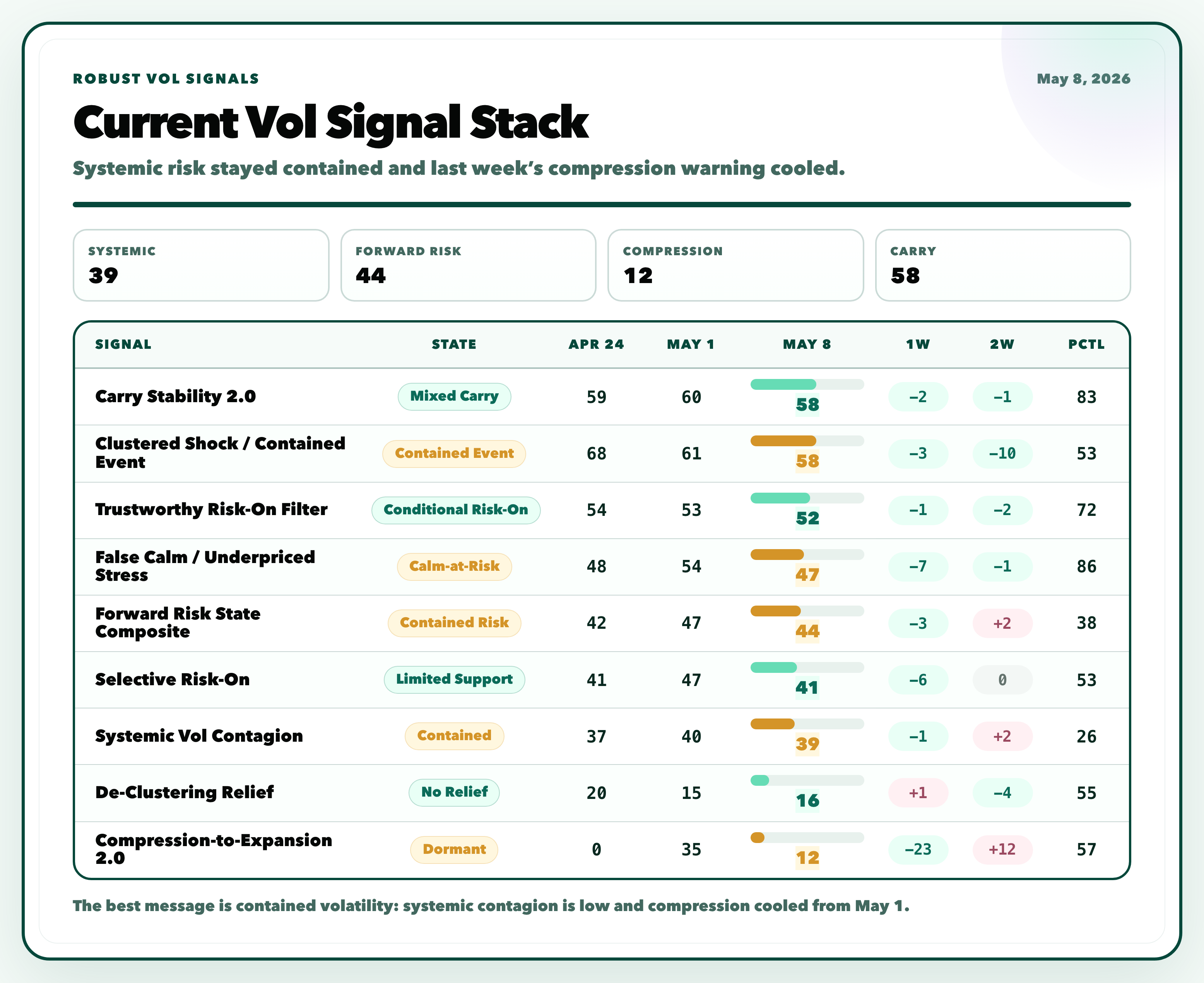

New Volatility Signal Stack

Here is the volatility signal stack through May 8, compared with the last two Fridays. To give you a quick description of the above is that the dangerous systemic volatility signals are not confirming a major warning.

Systemic Vol Contagion is still contained at 39. Forward Risk State Composite is only 44. Compression to Expansion fell from 35 to 12, which is the biggest improvement in the stack versus last Friday.

That’s important because last week the one signal that had my attention was compression waking up. This week, that warning cooled substantially. It is not back to zero, but it is no longer accelerating the way it was last Friday.

The remaining caveat is Calm at Risk. It fell from 54 to 47, which is good, but it is still elevated in percentile terms. I’m viewing that as more context rather than a regime breaker. It says do not call the setup completely risk free, but it does not override the broader contained vol message.

Realized Vol Co Stress

The realized vol co stress layer did also improve this week.

The average correlation fell, PC1 share fell, and the high correlation share fell. This means realized volatility is not becoming more synchronized across the whole market. There is still sector neutral stress under the surface, but most of the common movement still looks clustered rather than marketwide stress.

This is more consistent with contained/event-driven pockets of stress which I believe we do see in the market now as well.

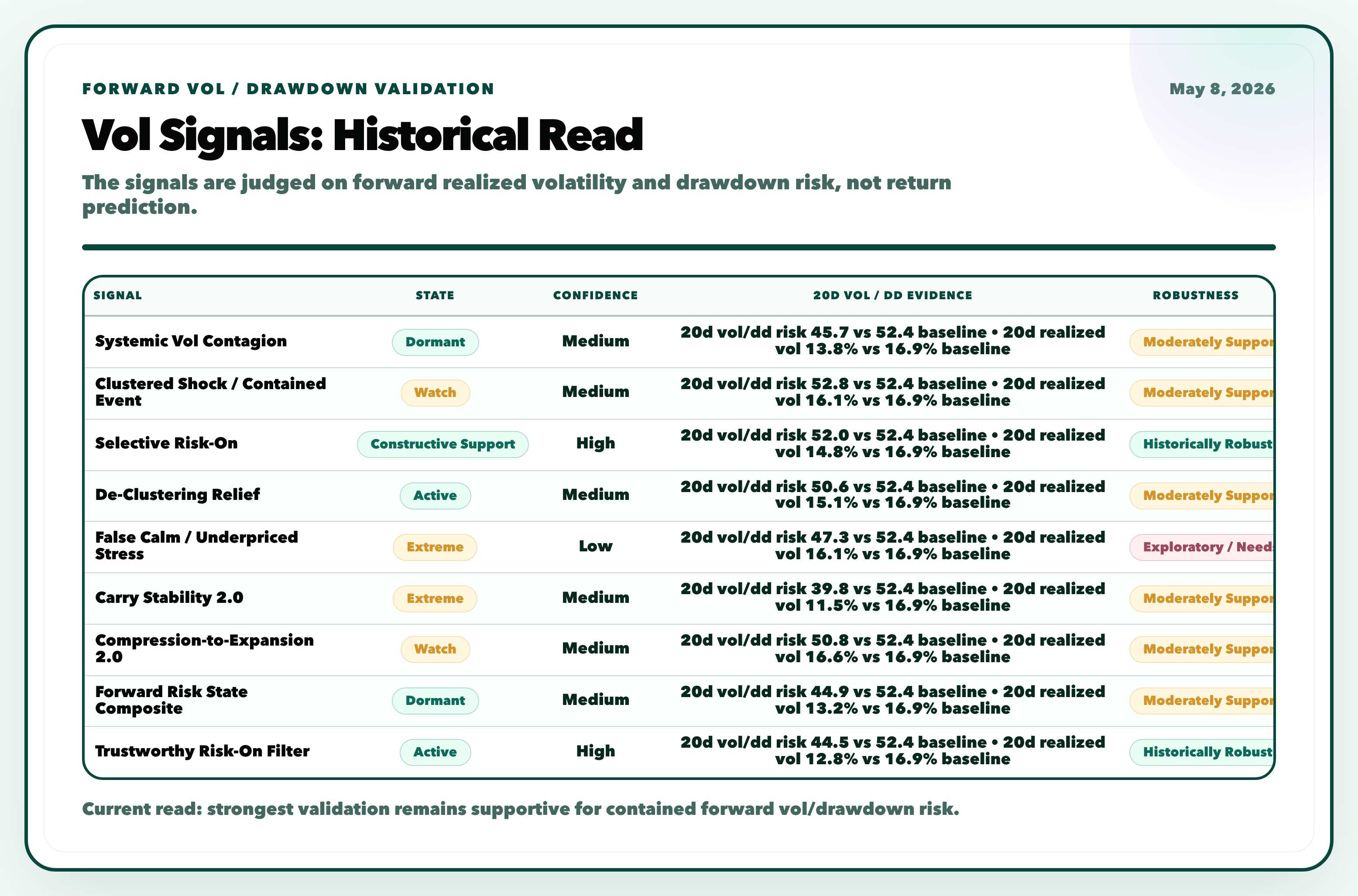

How The Vol Signals Have Tested Historically

The validation layer here is important because these signals are not being judged mainly on future returns. They are being judged on forward realized volatility and drawdown risk, which is the real objective of the volatility stack we use.

Current state validation reads are as follows in the above screenshot.

The important point is that the strongest and most useful signals are not in dangerous configurations right now. Carry stability, trustworthy risk on, forward risk, and systemic contagion are all pointing to lower or contained forward vol/drawdown risk versus baseline.

Compression to Expansion is still the one to monitor, but it cooled from last week and we would need to watch for either this reducing to 0 now or increasing again in the earlier part of next week.

Calm at Risk remains useful, but its current validation confidence is low, so I would not let it override our better and more robust supported signals.

Forward vol risk is present, but not dominant. A good way for us to interpret this is, contained volatility with selective fragility, not imminent systemic vol expansion. We know how quickly vol can expand however, and therefore, we will be watching the compression to expansion intently.

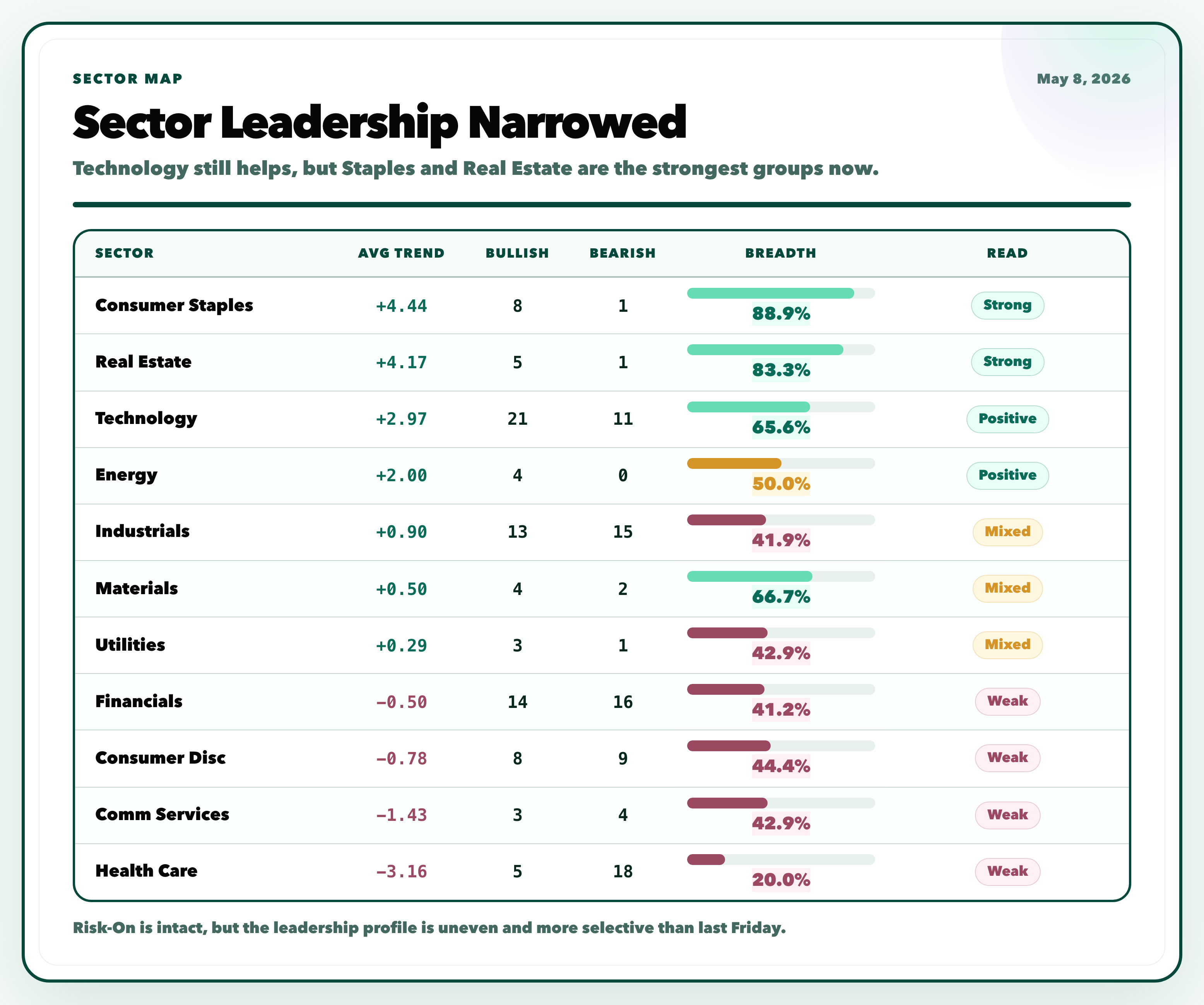

Sector Leadership

Sector leadership did narrow further this week. The strongest sector trends are now Consumer Staples, Real Estate, and Technology.

That is an interesting mix in my opinion. Technology remains constructive, which supports the Risk On read, but very dispersed. Consumer Staples and Real Estate are the two strongest sectors, which gives the leadership map a more defensive quality than a pure high beta Risk On tape.

The weaker areas are Health Care, Communication Services, Consumer Discretionary, and Financials. Health Care remains the clearest laggard. Financials and Consumer Discretionary weakening matters more than Health Care alone, because those areas are more connected to the quality of the broader risk on move.

Therefore, again Risk On is intact, but sector leadership is uneven. Technology is helping, but the tape is not broadly high beta and did get a bit messy this week.

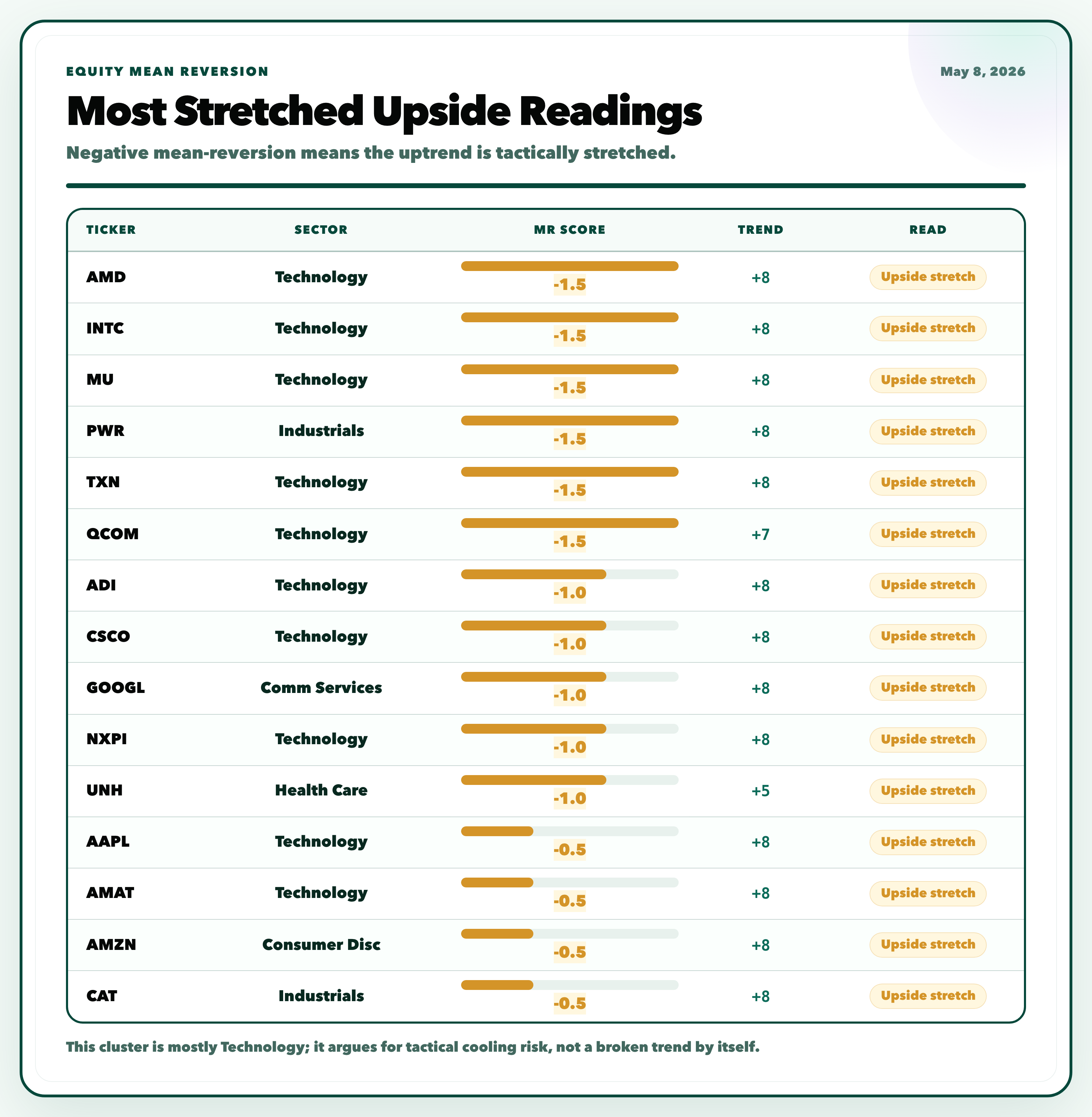

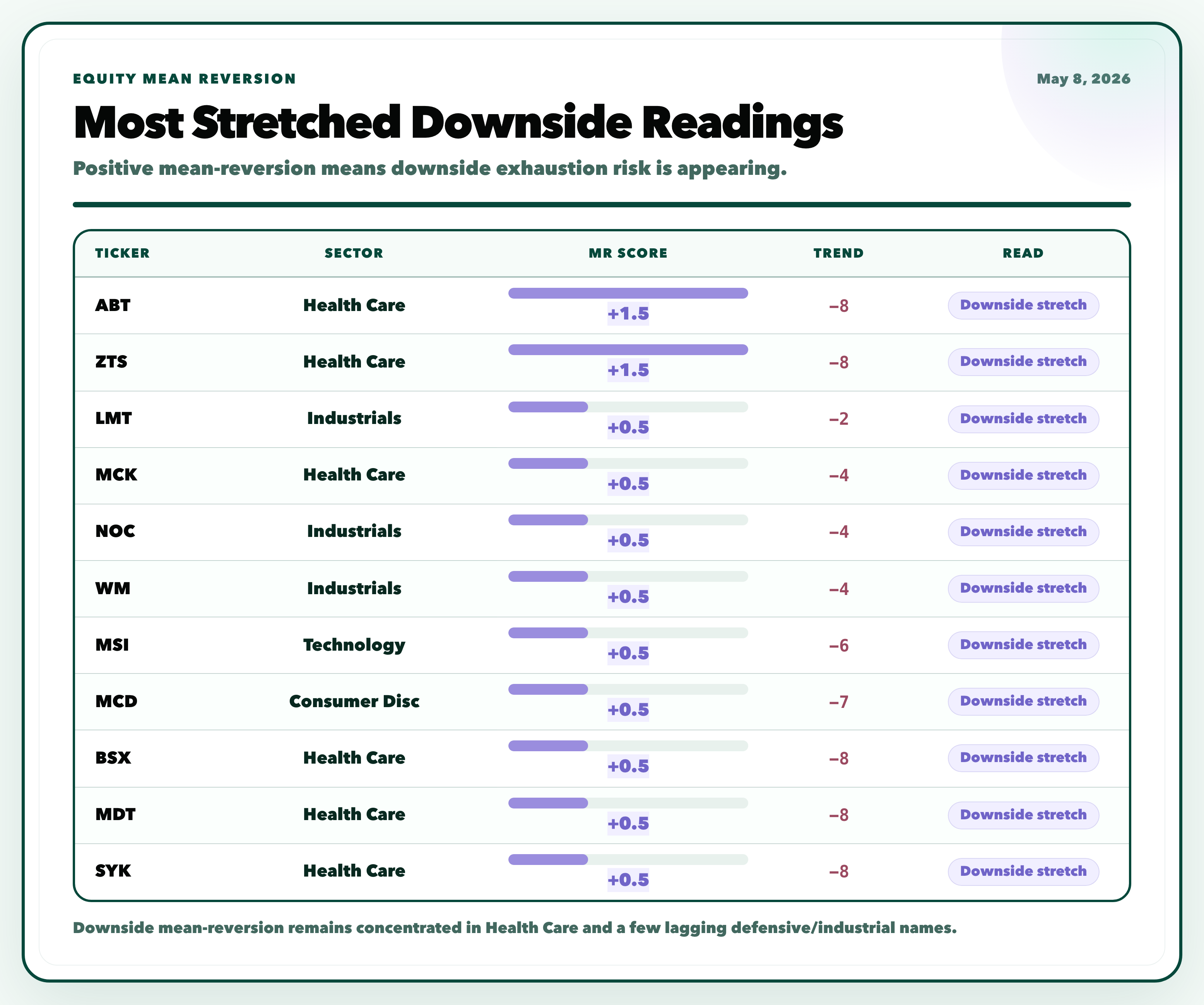

Mean Reversion Signals

Mean reversion activity increased again this week. The regime model now shows 39 mean reversion signals, up from 35 last Friday and 31 two Fridays ago.

The upside stretch is mostly in Technology, which makes sense given the sector remains one of the stronger areas. The downside stretch is still heavily concentrated in Health Care.

In a Risk On regime, mean reversion signals often mean cooling inside an intact trend. But the increase from 31 to 35 to 39 over the last two weeks does say the market has more stretched pockets under the surface. One note is the half life here, some of these are deteriorating due to that and if they do not revert this week I imagine signal wise they will become very weak. This is a problem for next, however, we’ll see. If any mean reversion signals are taken I would personally take profits on them quickly.

Interpretation

The full signal stack is still positive, but less clean than last Friday and bit messier in my opinion.

The constructive side is clear:

The main regime model remains Risk On with 95 confidence.

Aggregate score improved again to 78.

Macro score improved sharply to 106.

Average IV percentile eased to 37.

Historical regime proxy is Risk On.

SPY realized vol percentile fell to 37.

Median VRP remains positive at 0.53.

Negative VRP share remains 0.0%.

Systemic Vol Contagion is contained at 39.

RV co-stress improved from 54 to 46.

Compression to Expansion cooled from 35 to 12.

⠀The caution side is also clear:

Stock breadth fell from 55 to 48.

Sector breadth fell from 69 to 60.

Mean reversion signals rose from 35 to 39.

Sector leadership is uneven.

Consumer Staples and Real Estate are leading more than classic high beta areas.

Calm at Risk is still elevated in percentile terms.

Compression to Expansion even though it cooled, it’s still not at 0.

The correct interpretation is not “everything is perfect.” It is also not “the market is rolling over.”

We should remain as Risk On remains the base case, but it has become more selective. Volatility is contained, systemic stress is not spreading, and the main vol warning from last week cooled. But breadth narrowed, so the market needs participation to improve again for the setup to feel cleaner, Mean Reversion signals need clearing out sooner rather than later, some vol signals need to reduce as well. I would also say let’s watch if we get reversion in semi’s and how the broader market reacts to that reversion. This will be an interesting tell as well.

What Would Change The Signal View

The current view would become more defensive if we saw the following

Stock breadth staying below 50 or deteriorating further. Breadth fell from 55 to 48 this week. A quick recovery back above 50 would help. Further weakness would make the Risk On regime lower quality.

Systemic Vol Contagion moving into the 50s or 60s. It is currently 39, so this is not happening yet.

Compression to Expansion reaccelerating. It fell from 35 to 12, which is good. If it moves back above last week’s level, the vol warning returns.

Forward Risk State Composite moving above 60. It is currently 44, so forward risk remains contained.

RV co stress moving back above 55 to 60. The composite improved to 46. A reversal would suggest volatility is synchronizing again.

Weakness spreading into Technology. Technology is one of the reasons Risk On still holds. If Technology breadth breaks, the signal stack would look much worse.

Financials and Consumer Discretionary failing to recover. Both are already soft. More weakness there would make the risk-on tape less durable.

Calm at Risk rising while the stronger validation signals also worsen. Calm at Risk alone is context. Calm at Risk plus rising systemic contagion or rising forward risk would matter much more.

Conclusion

The market remains Risk On, and volatility risk is still contained but there are a few tiny signs under the surface.

The best news this week is that the main vol warning from last week cooled. Compression to Expansion fell from 35 to 12, realized vol co stress fell from 54 to 46, and systemic vol contagion remains contained at 39.

That all means volatility is not currently confirming a broad market deterioration.

The less clean part is breadth which disappointedly weakened further after last week’s increase. Stock breadth fell back below 50, sector breadth fell, and mean reversion stretch increased.

For now, the best read from all above is to stay positive while the Risk On regime, macro trend, and contained vol signals remain intact, but respect the narrowing breadth and some tiny vol signals. The setup is not screaming systemic risk, but it is also not a full breadth all clear, especially with the current Mean Reversion signals.

The interesting aspects to watch this week will be if those Mean Reversion signals react and what will be the broader markets move in accordance with that as well. Therefore, let’s monitor that as well and if you take the reversion signals, act quickly on them. Furthermore, watching for any reaccelerating in the Compression to Expansion signal will be a wise move as well.

Thanks as always for reading, and have a great rest of your night. Please reach out if any questions or feedback. Thanks again